So you’ve just received your first ever salary from your first full-time job. Chances are, it’s much higher than the monthly allowance you’ve gotten from your parents or even during National Service. In your excitement, you start listing down all the things you’re going to spend it on: more office clothes, dinner treats for your family and friends, Grab-ing everywhere you go and perhaps even making daily trips to Starbucks for your caffeine boost instead of your cheap 3-in-1 coffee at home.

Life sounds good, right? That is, until you check your bank statement at the end of the month, and realise that you’ve spent much more than expected. Unfortunately, your first salary is not infinite, and your financial responsibilities will only grow as time goes on. If you don’t want to live from paycheque to paycheque, or worse, spiral into debt, you need to quickly adopt some healthy budgeting skills to keep you on track to financial independence.

Know your goals

Yes, everyone’s goal in life is to have more money, but take the time to understand your long-term financial goal in life. Start with a target to aim for when managing your money. Whether it’s just ensuring you don’t get into debt or saving part of your salary every month, it’s more effective to have a concrete goal to work towards, no matter how basic it is. It’s fine to start with a low bar with your first few paycheques as long as you stick to your goal.

Similarly, it’s fine to have some loftier ambitions for the long run, such as saving up for your own place or retiring in the Bahamas in the next 20 years. Just be sure to revisit these goals whenever your financial situation changes, such as if you get a pay raise or if you need to settle additional expenses.

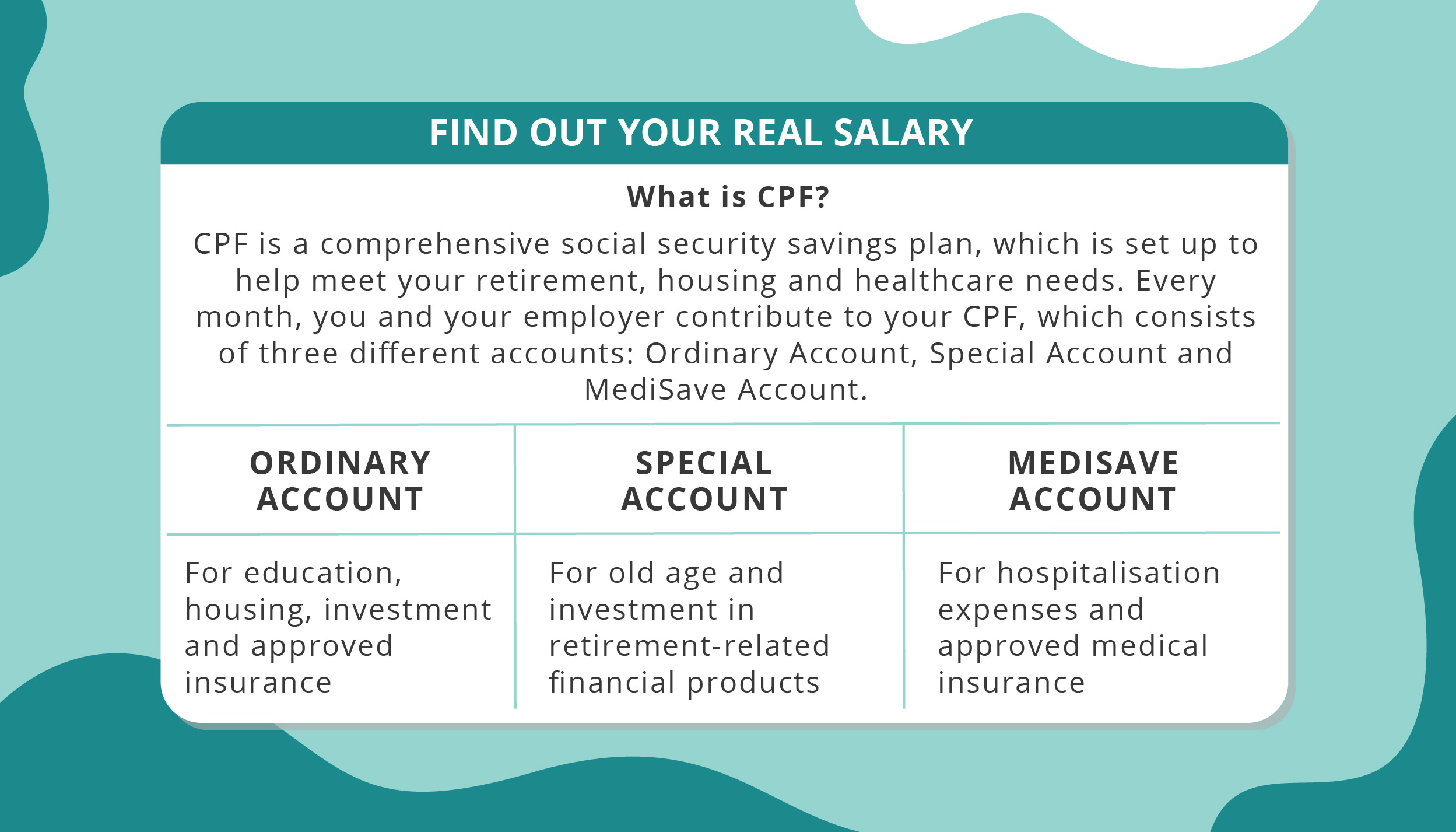

Find out your real salary

Just because your salary is stated as S$4,000 per month, doesn’t mean you’re getting every cent of it into your bank account. There is an automatic monthly employee’s contribution requirement of 20 per cent from your salary, which means S$800 will be deducted from your pay each month and be deposited to your Central Provident Fund (CPF) account. Your take-home pay is thus S$3,200. When you’re planning your budget and expenses, be sure to always base it on your take-home page, not your gross salary.

Choose a budget that suits you

There are many budgeting tips out there, so you may need a couple of tries before finding out what works for you. The easiest way is to download an app to your phone and keep track of all your spending habits. Only then will you realise that if you keep buying that vanilla latte every morning on your way to the office, your monthly coffee habit can easily shoot up to S$100 a month (and that doesn’t even include breakfast).

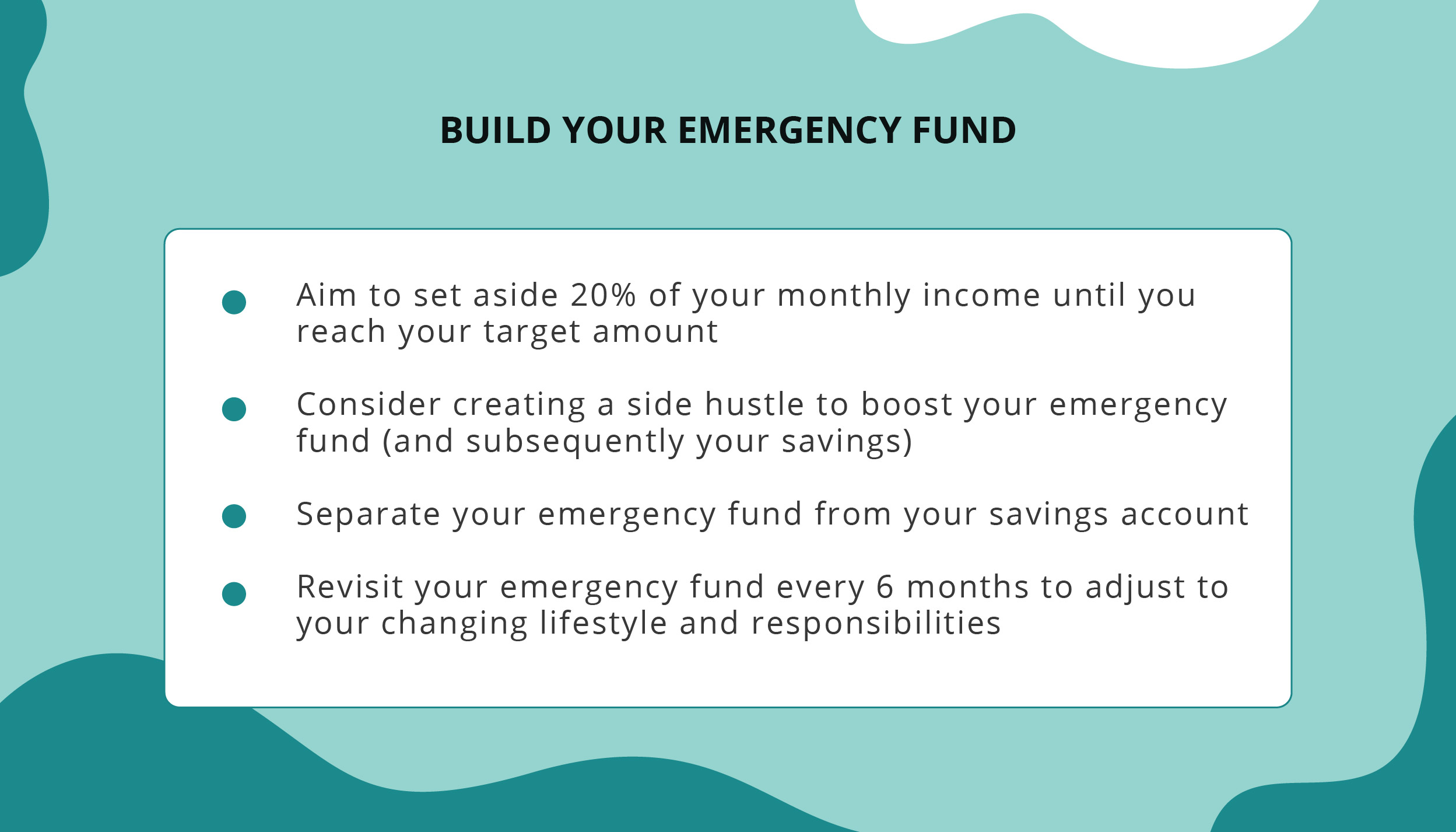

Have an emergency fund

For those who think it’s fine to live from paycheque to paycheque just to enjoy that daily artisan coffee, it’s a scary way to live, and this philosophy goes against the belief of every financial expert out there. It’s fine to do it for your first few salaries; perhaps you need to repay your student loan or upgrade your workstation at home if you’re working remotely. But it’s certainly not a sustainable financial habit. Make sure you have at least 3 to 6 months’ worth of expenses in your emergency fund, which is separate from your savings. An emergency fund is readily available cash in case you need to pay a sudden expense, while savings is a long-term goal.

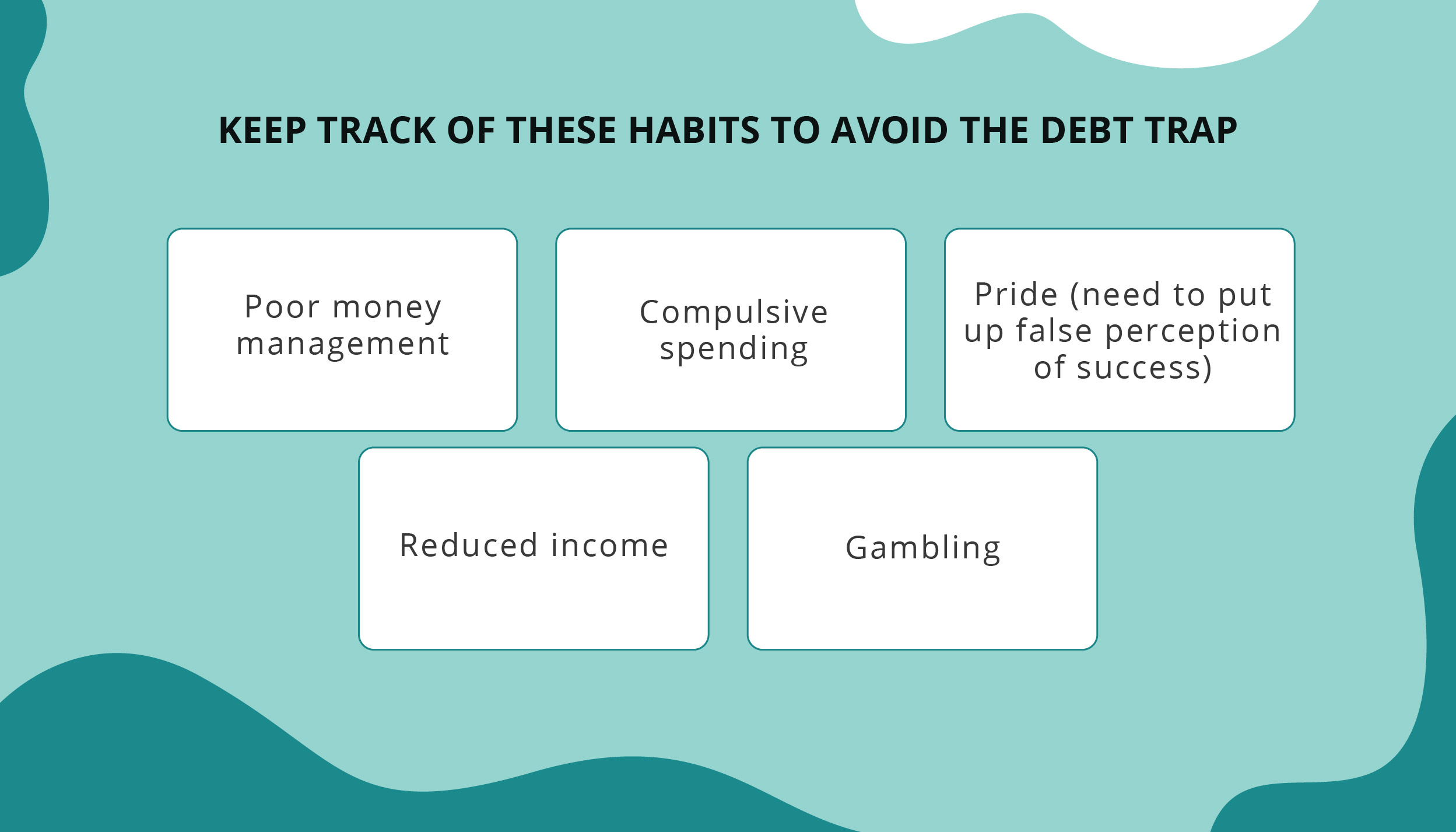

Don’t fall into the debt trap

At this point, the only debt you should be paying off is your school loans. Don’t allow yourself to pick up more debts and always spend within your means. Remember, debt tends to accumulate itself, and you should be doubly careful when you get a credit card. After all, the average credit card interest rate is about 20-25 per cent, so imagine how much more you’ll have to pay off your bill if you’re unable to make the full payment at the end of the month.

Always invest in yourself

If you decide to be frugal, however, don’t take it to the extreme. Living life on the bare necessities won’t maximise your potential savings, and it’ll just make you miserable in the long run. After all, even if you just resort to cheap food and staying in all day under the pretense of saving money, you’d be hard-pressed to say that you’re living a meaningful life.

Creating a budget that works for you doesn’t have to be rocket science, and you don’t have to live a miserable life just to build up on your savings. As long as you develop on a reasonable budget plan and stick to it, especially from your first paycheque, you’ll be good to go.